How Are Capital Markets Projections Constructed?

Guiding objectives and process

Underlying beliefs guide the development of the projections

- An initial bias toward long-run averages

- A conservative bias

- An awareness of risk premiums

- A presumption that markets are ultimately clear and rational

Reflect our beliefs that long-term equilibrium relationships between the capital markets and lasting trends in global economic growth are key drivers to setting capital markets expectations

Long-term compensated risk premiums represent “beta”—exposure to each broad market, whether traditional or “exotic,” with limited dependence on successful realization of alpha

The projection process is built around several key building blocks

- Advanced modeling at the individual asset class level (e.g., a detailed bond model, an equity model)

- A path for interest rates and inflation

- A cohesive economic outlook

- A framework that encompasses Callan beliefs about the long-term operation and efficiencies of the capital markets

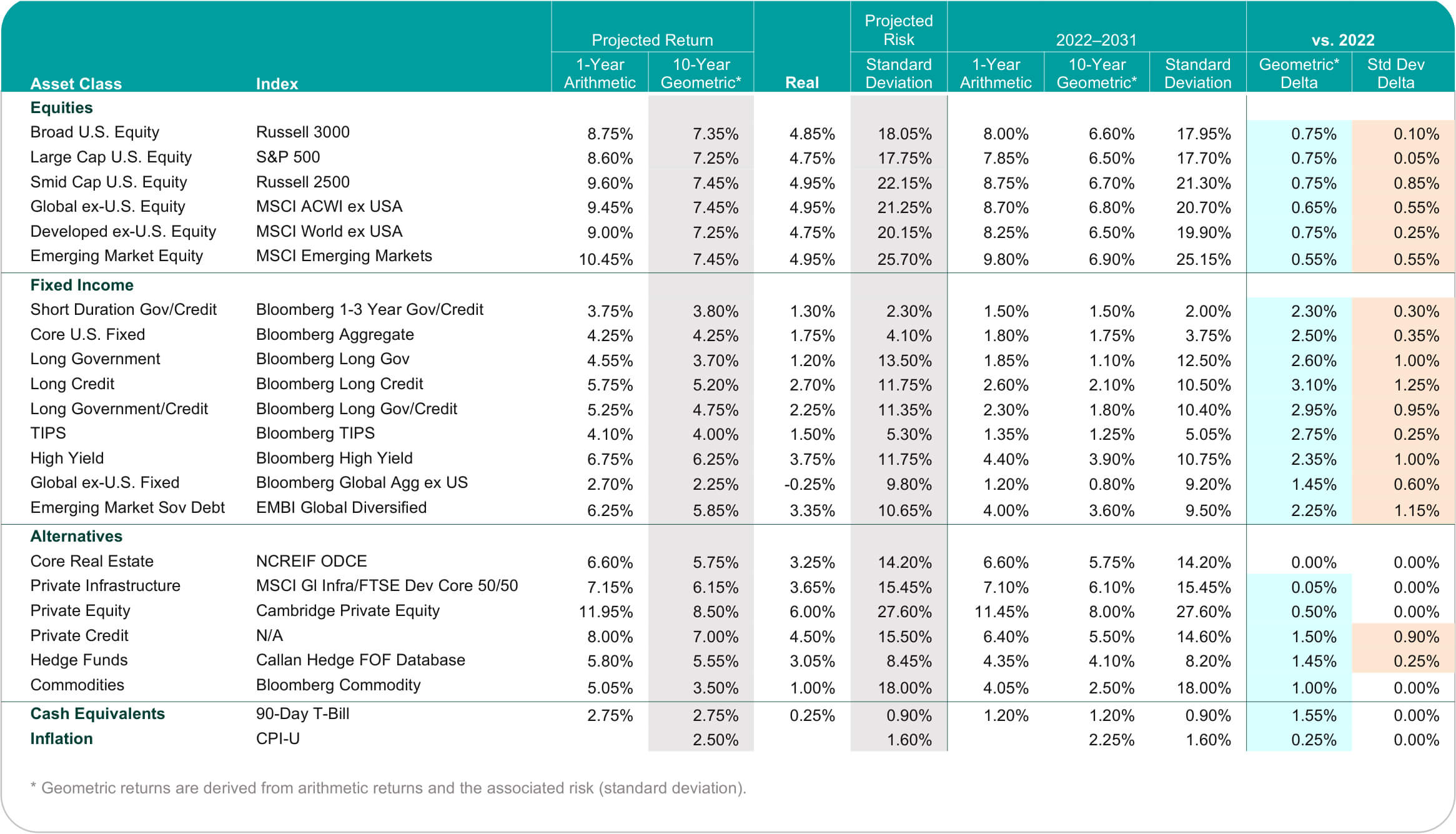

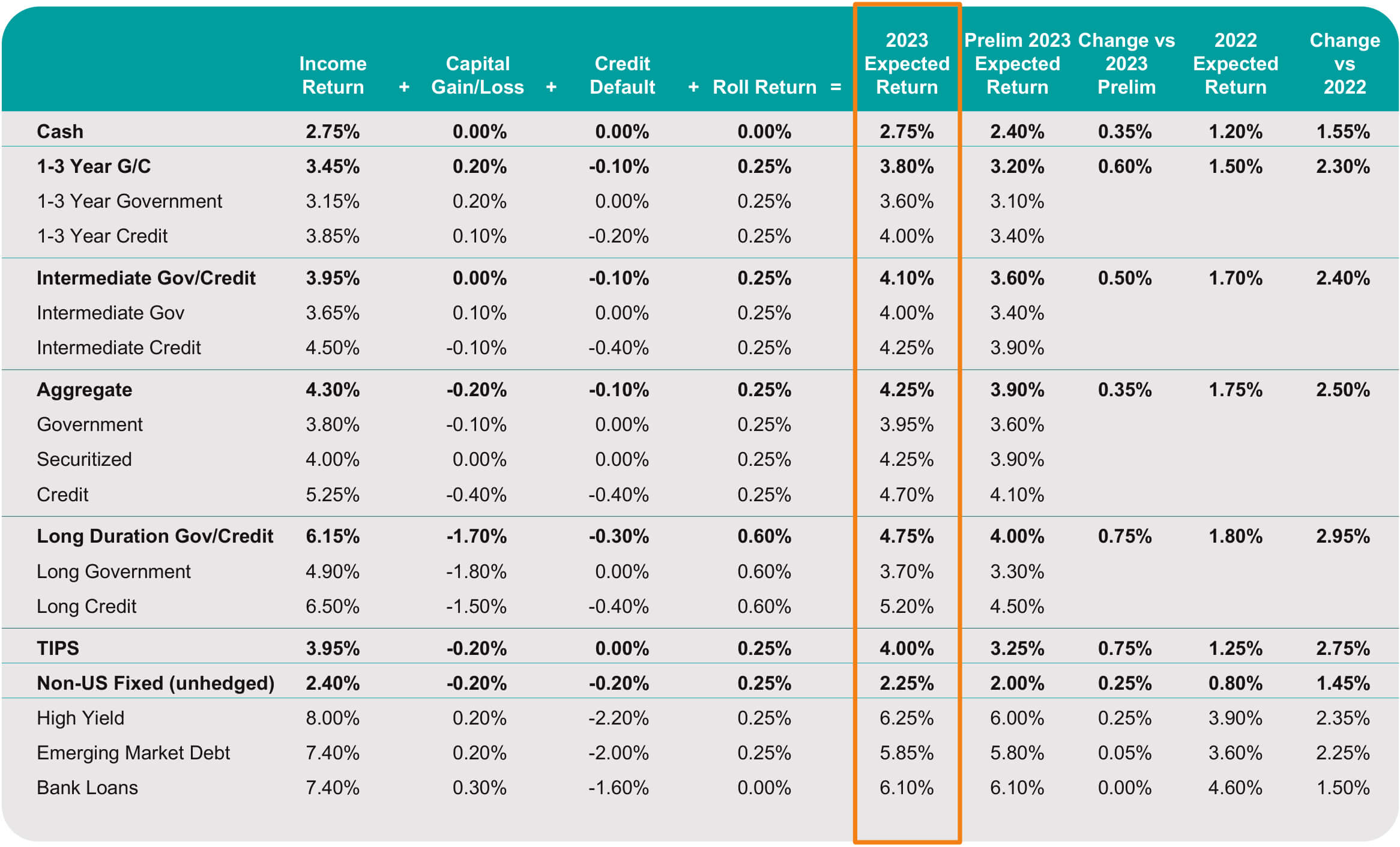

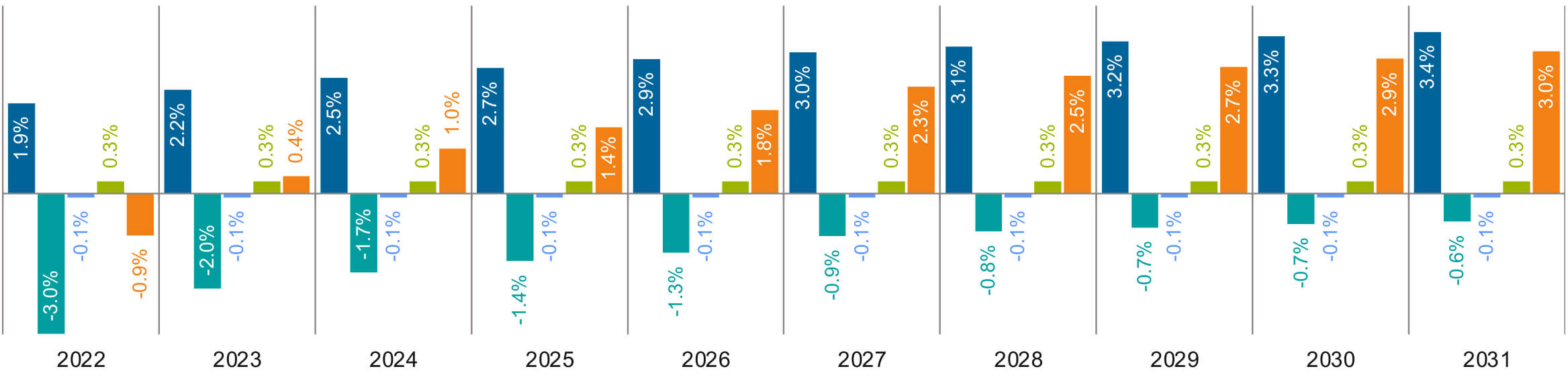

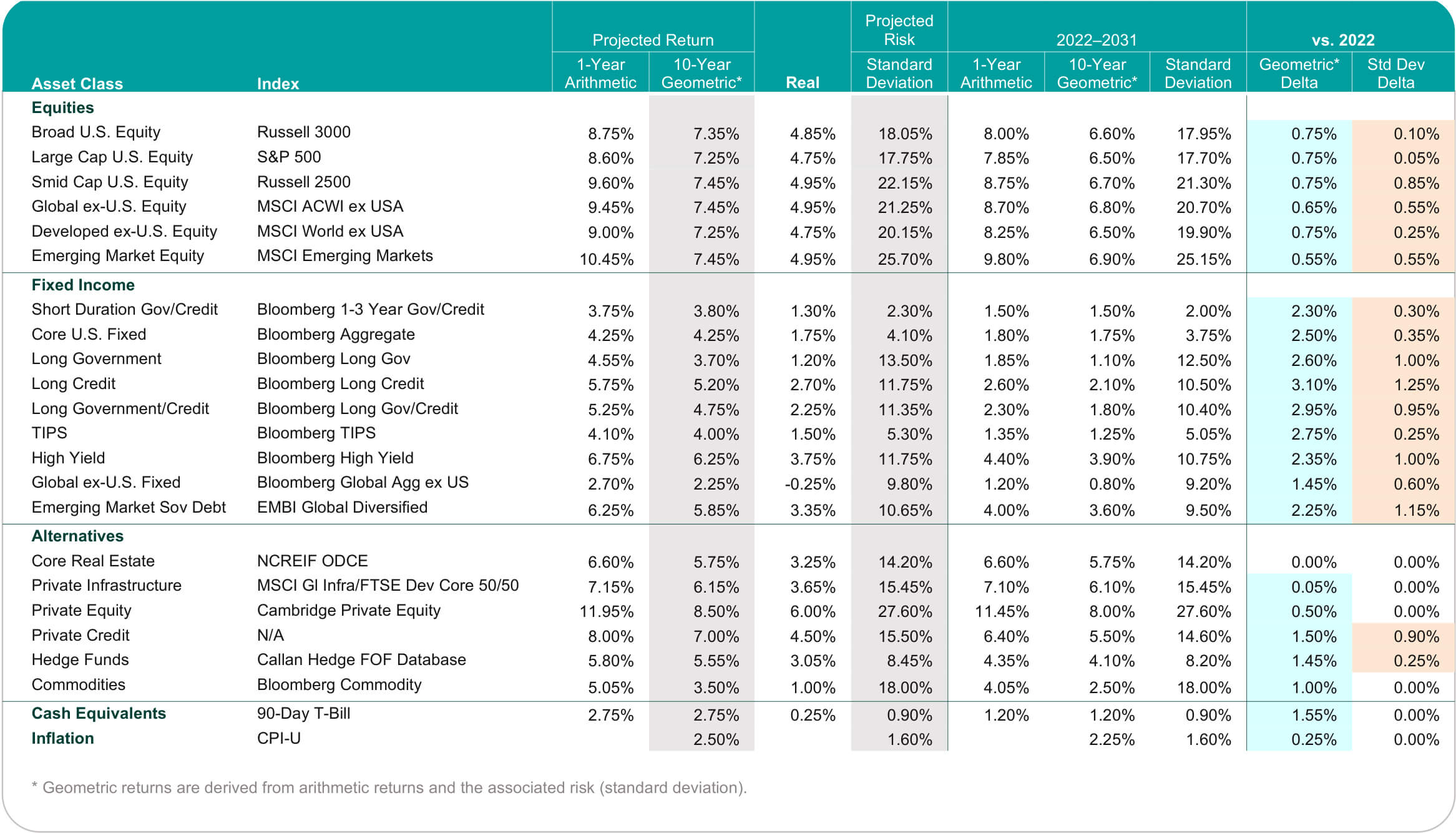

2023 vs. 2022 Risk and Returns Assumptions

Summary of Callan’s Long-Term Capital Markets Assumptions (2023–2032)

Current Market Conditions

Equity and Fixed Income Markets Down Together in 2022

Negative returns for stocks and bonds at the same time for three quarters are extremely unusual

Global equity markets down sharply in 2022 despite rebound in 4Q

Similar impact across all equity market segments: developed, emerging, small cap

Fixed income down with sharply higher inflation and interest rates

Bloomberg Aggregate: -13% for the year, worst year ever for the index by a wide margin

CPI-U: +6.5% for the year ended Dec. 2022

- Number of times stocks and bonds have been down together

- 38 quarters in almost 100 years, about 10% of the quarters

- But just twice on annual basis

- Inflation at highest rate in decades

- Economic data show growth hit ‘pause’

- GDP rose 3.2% in 3Q22 after falling in both 2Q and 1Q; consensus estimate is 1% for 4Q

- Forecasters have cut growth estimates for 2022 close to 0%, and to 1.5% for 2023.

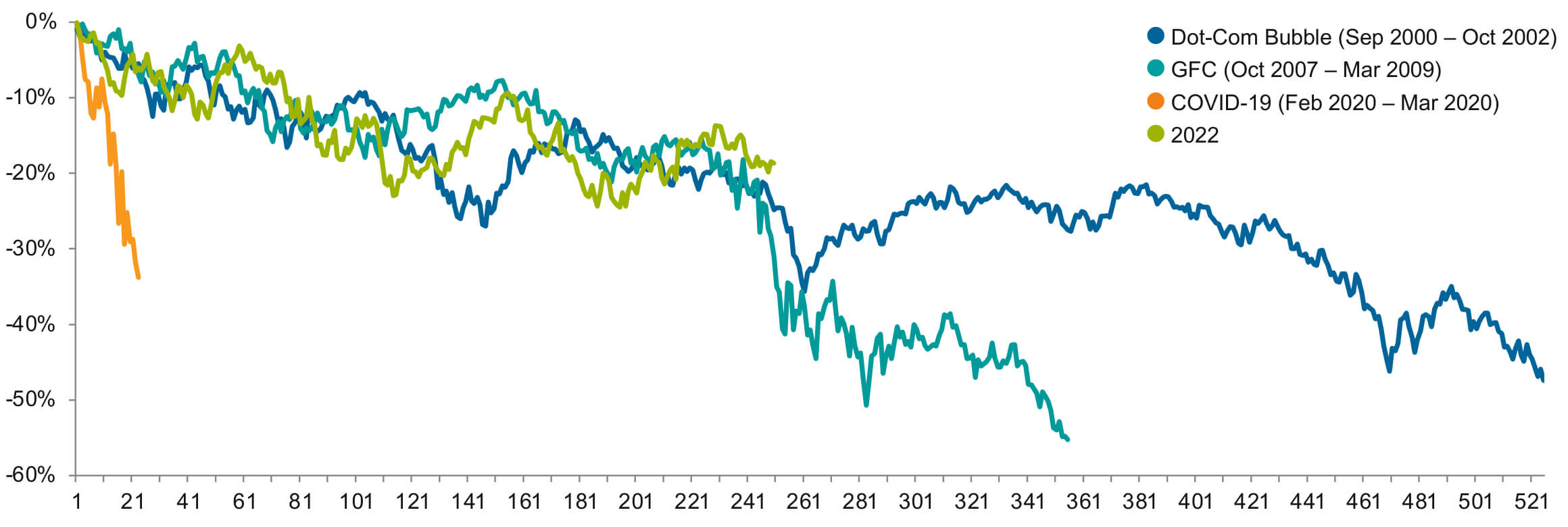

2022 Equity Drawdown: A More ‘Typical’ Correction?

S&P 500 Cumulative Returns

Market Peak-to-Trough for Recent Corrections vs. 2022 Through 12/31/22

Trading Days From Market Peak

- While the COVID correction was swift and intense, the 2022 correction resembles the GFC and Dot-Com Bubble.

- The 2022 drawdown has been 250 trading days through December.

- It would take another 105 trading days to get to the bottom of the GFC and 275 trading days to get to the bottom of the Tech Bubble.

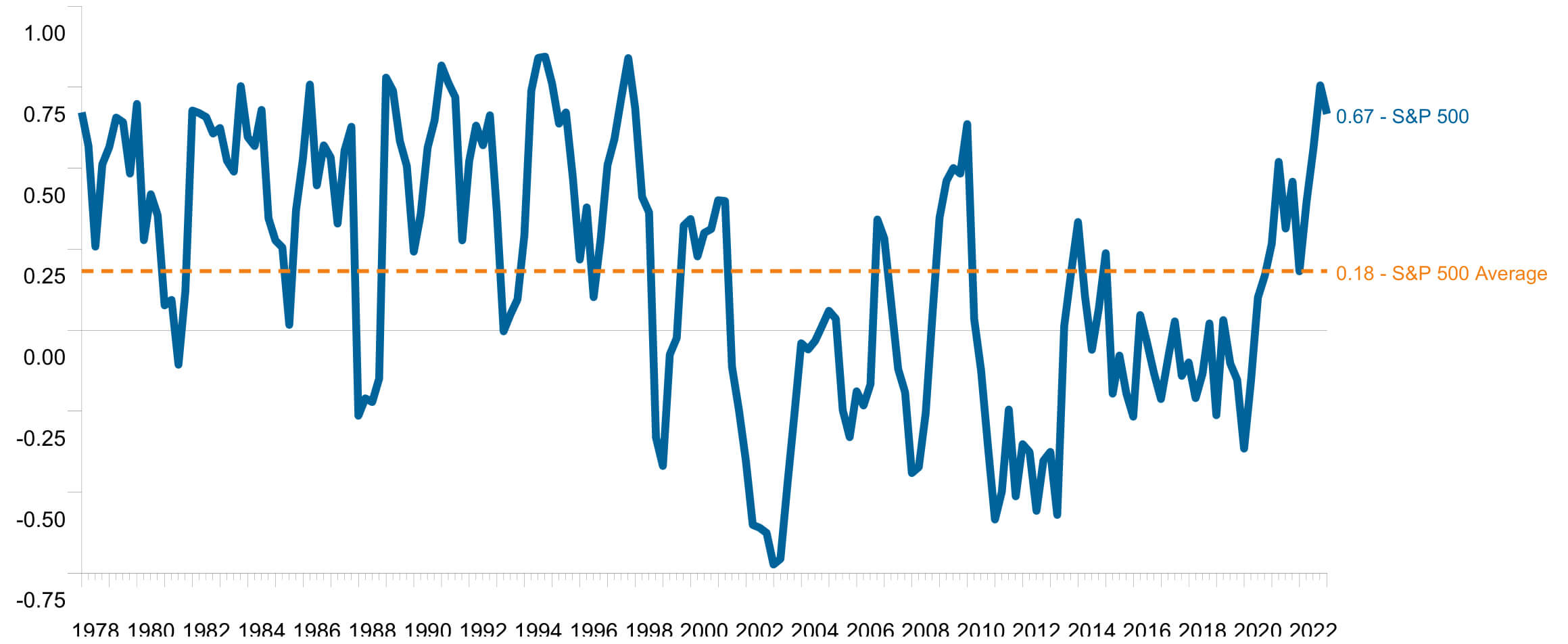

Did Diversification Fail in 2022?

Stocks and bonds down together in each of the first three quarters of 2022; up together in 4Q22

Rolling 1 Year Correlation of S&P 500 to Bloomberg Aggregate for 45 Years Ended 12/31/22

Are we seeing a return to a regime of higher correlation between stocks and bonds, potentially lessening the diversification benefit of bonds to stocks?

10-Year vs. 2-Year Treasury Spread

- The 10-year to 2-year Treasury spread went negative two days in April and has been negative for most of 3Q and 4Q.

- Inversion in this spread does not always forecast a recession, but most recessions are preceded by a yield curve inversion.

- Yield curve inversion means investors expect a recession will occur and that interest rates will be cut, and therefore increase their demand for securities with longer duration, and therefore a higher potential for capital gain when rates fall.

- The 10-year Treasury to cash spread turned negative, which may be a better indicator of whether recession has already struck.

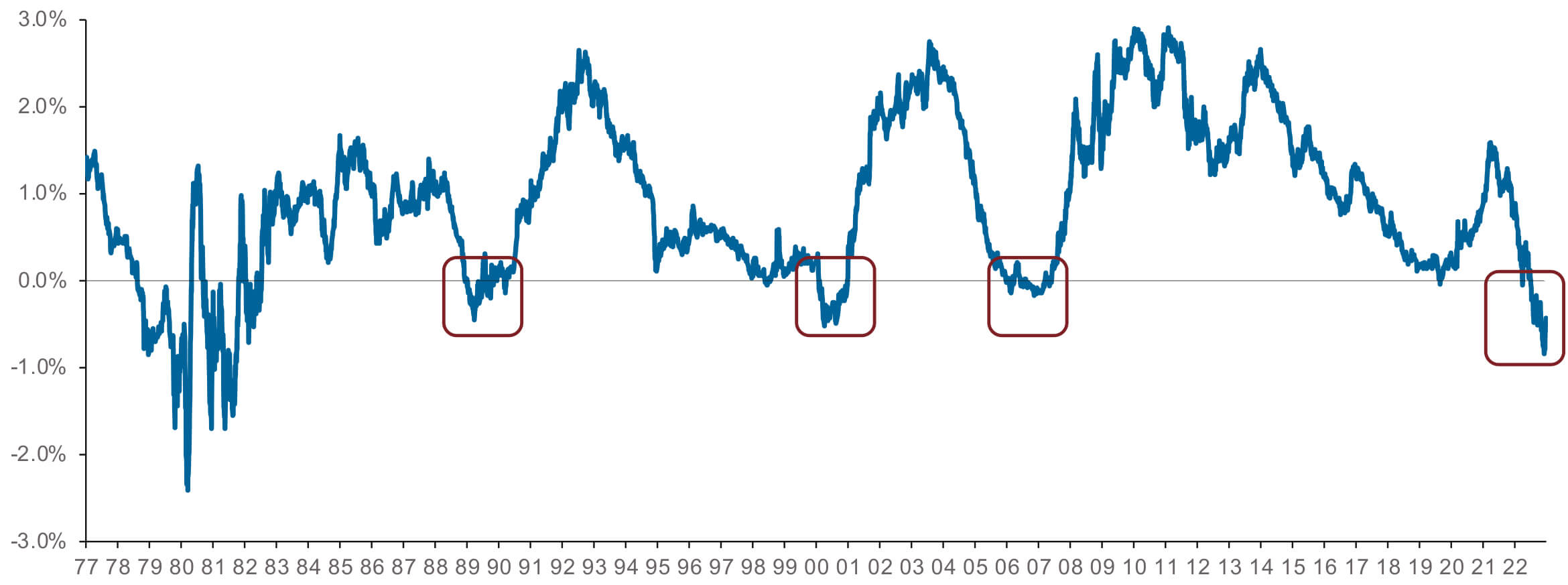

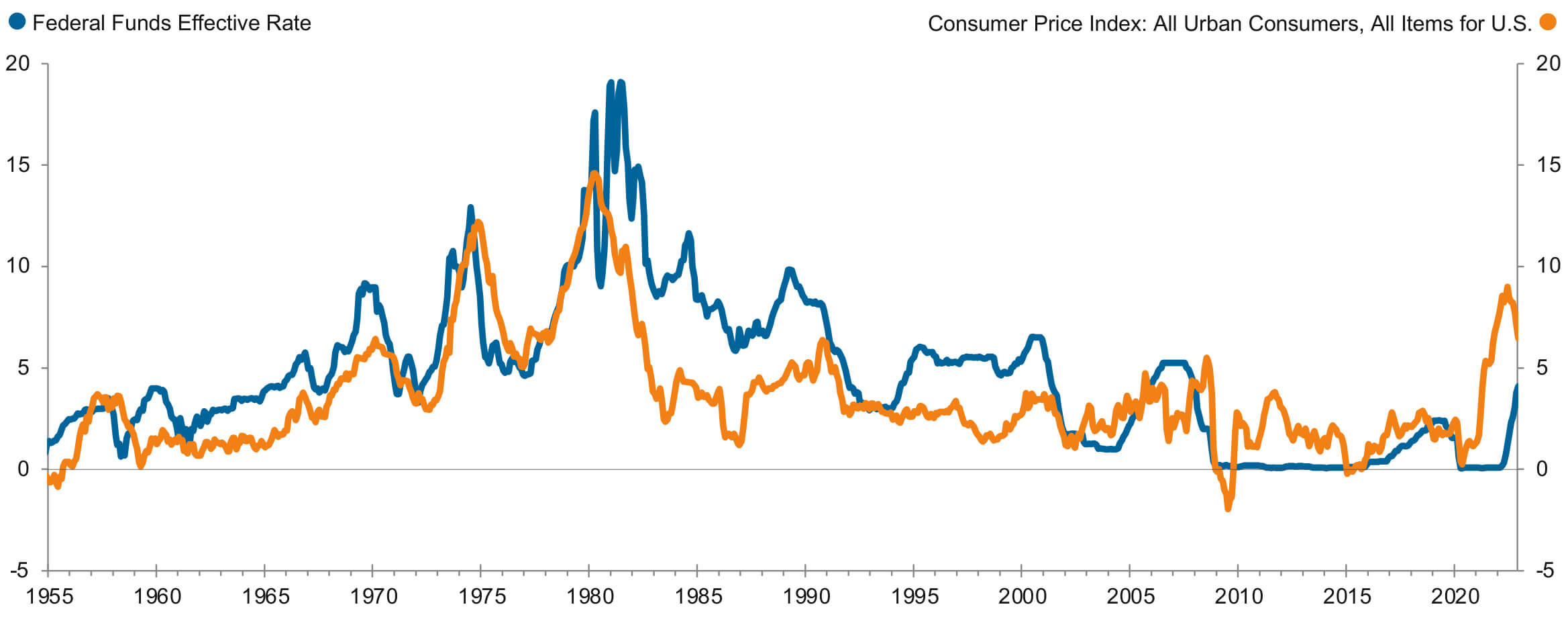

Inflation vs. Interest Rates Over the Long Term

Federal Funds vs. Consumer Price Index

- We are now looking at an inflation spike that is above the last rise in inflation from 2005–08.

- The gap between inflation and the Fed Funds rate is larger than that seen just before the GFC.

- Yield history suggests that the Fed Funds rate is typically above inflation, not below it.

- Recent gaps between CPI and the Fed Funds rate are unprecedented in the history of the CPI-U, going back to 1955

- Resolution to the historical relationship requires the Fed Funds rate to rise and inflation to fall.

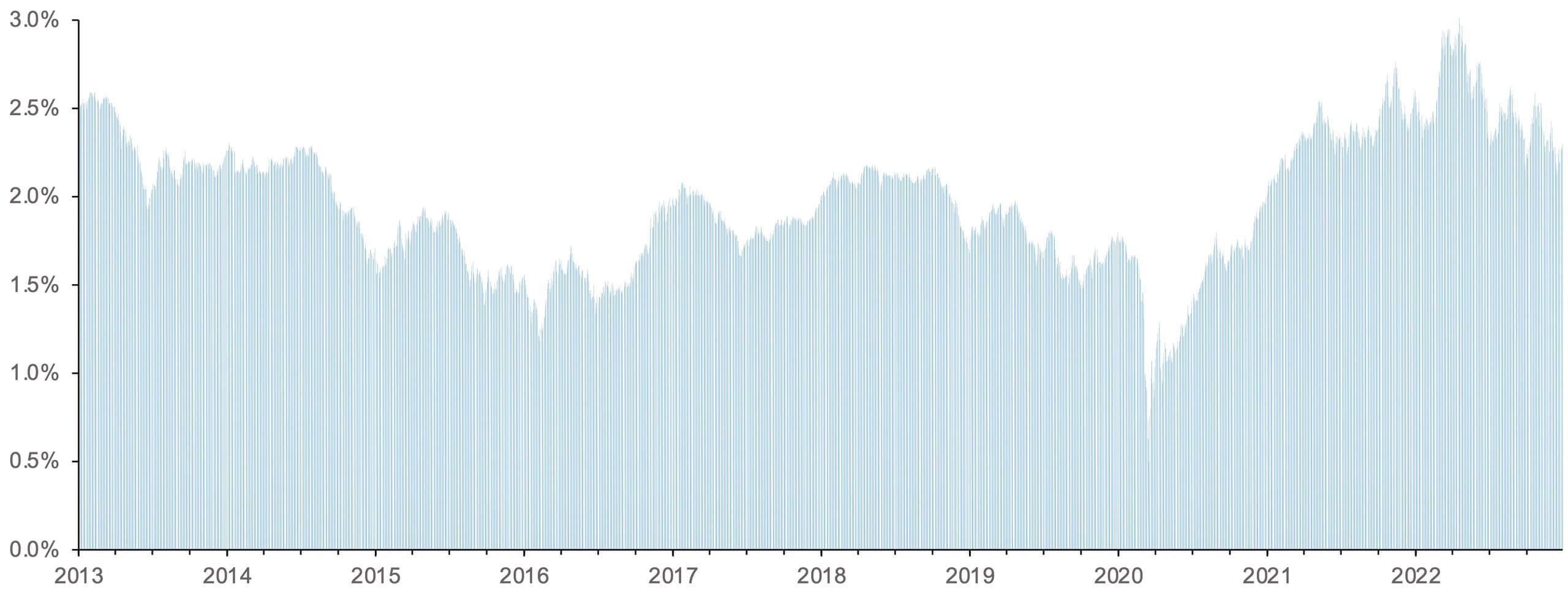

10-Year Breakeven Rate: Bond Market Forecast of Inflation

10-Year Breakeven Inflation Rate

- 10-year breakeven inflation rate is the difference in yield between the nominal 10-year Treasury and the 10-year Treasury Inflation-Protected Security (TIPS).

- Extra yield nominal Treasury would have to earn to maintain the same purchasing power as a TIPS investment.

- Values of implied inflation reached 3% in April but have since declined below 2.5%.

- Includes current high levels of inflation.

Fixed Income

10-Year Expected Returns

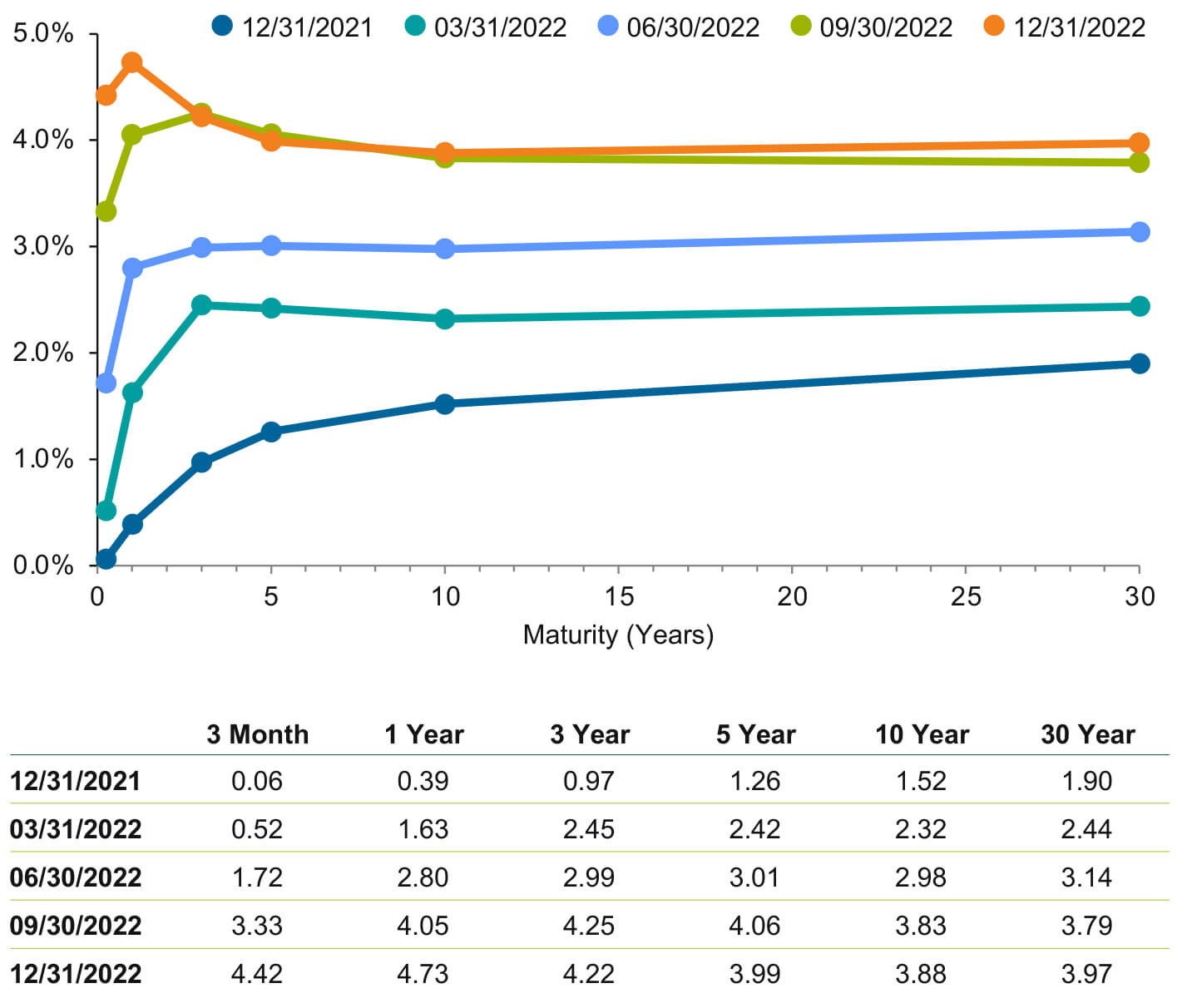

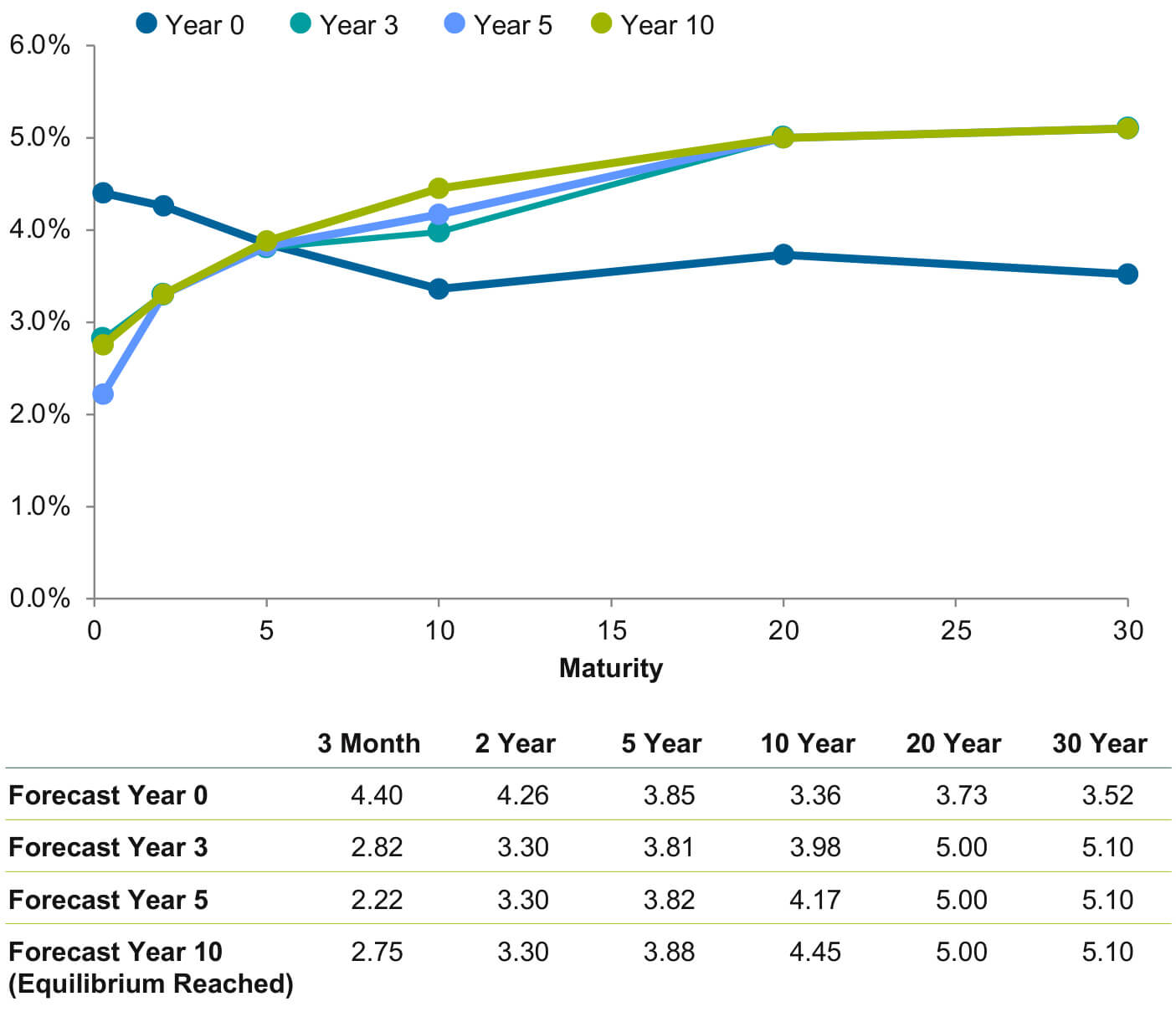

Yield Curve Continued to Rise and Became Inverted in Second Half of 2022

Rising yields throughout 2022 brought capital losses across bond indices.

Higher yields would lead to higher future returns, especially if yields stay at elevated levels.

Treasury Yield Curve Change

Shape of Yield Curve at Different Points in Forecast Horizon

Our forecast has the yield curve steepening within the first few years.

With yields already high, we expect yields to reach equilibrium by year 10 of our forecast (vs. year 30 in prior forecasts).

Yield Curve Forecast

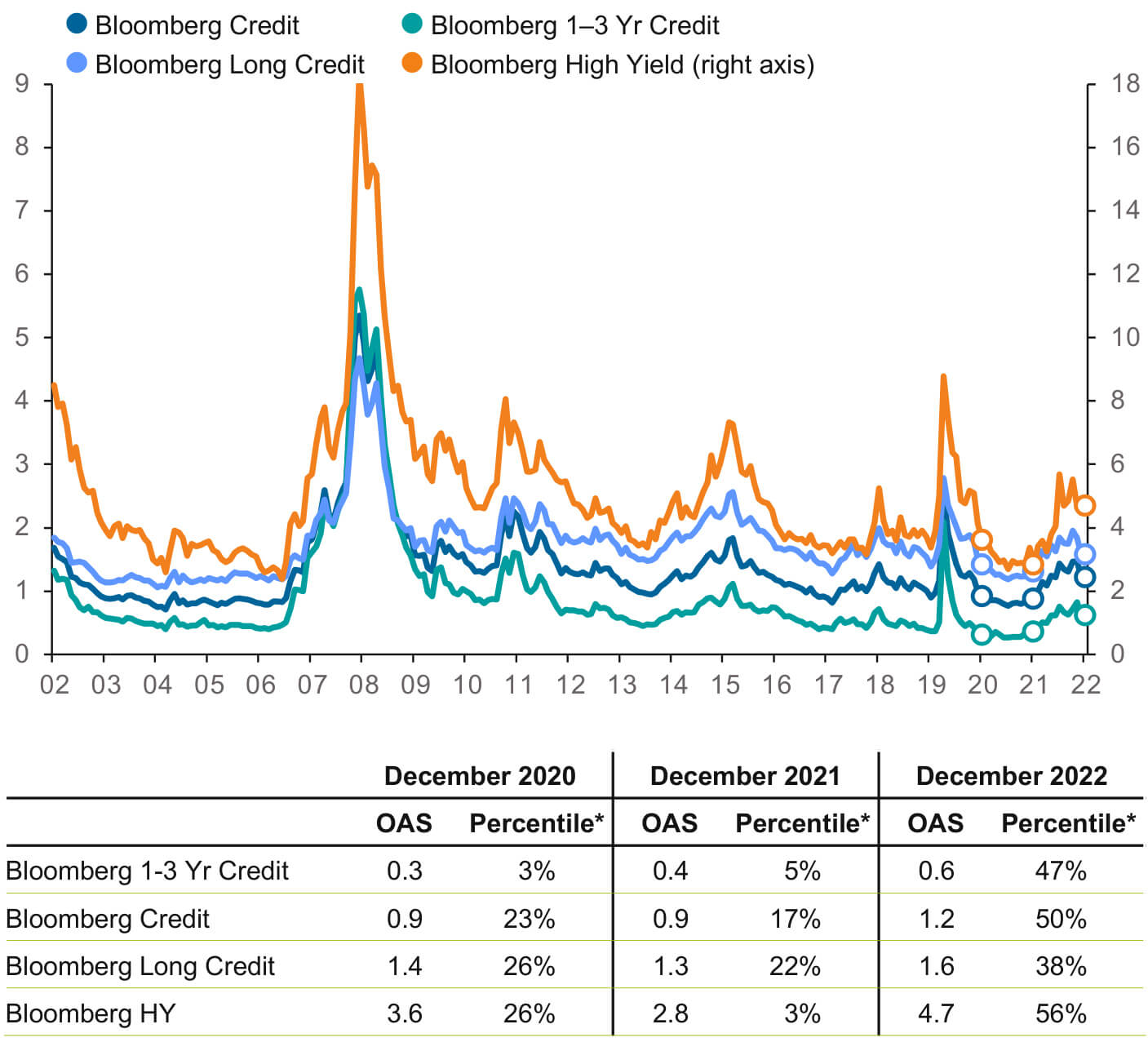

Spreads Dipped Through 2021 but Returned Toward Medians Throughout 2022

20 years ending 12/31/22

2022 projections had risk-free rates rising and credit spreads widening, creating twin headwinds for expected returns, especially for high yield.

After falling throughout 2021, credit spreads rose in 2022 and are closer to median in many cases.

Historical Option-Adjusted Spreads (OAS)

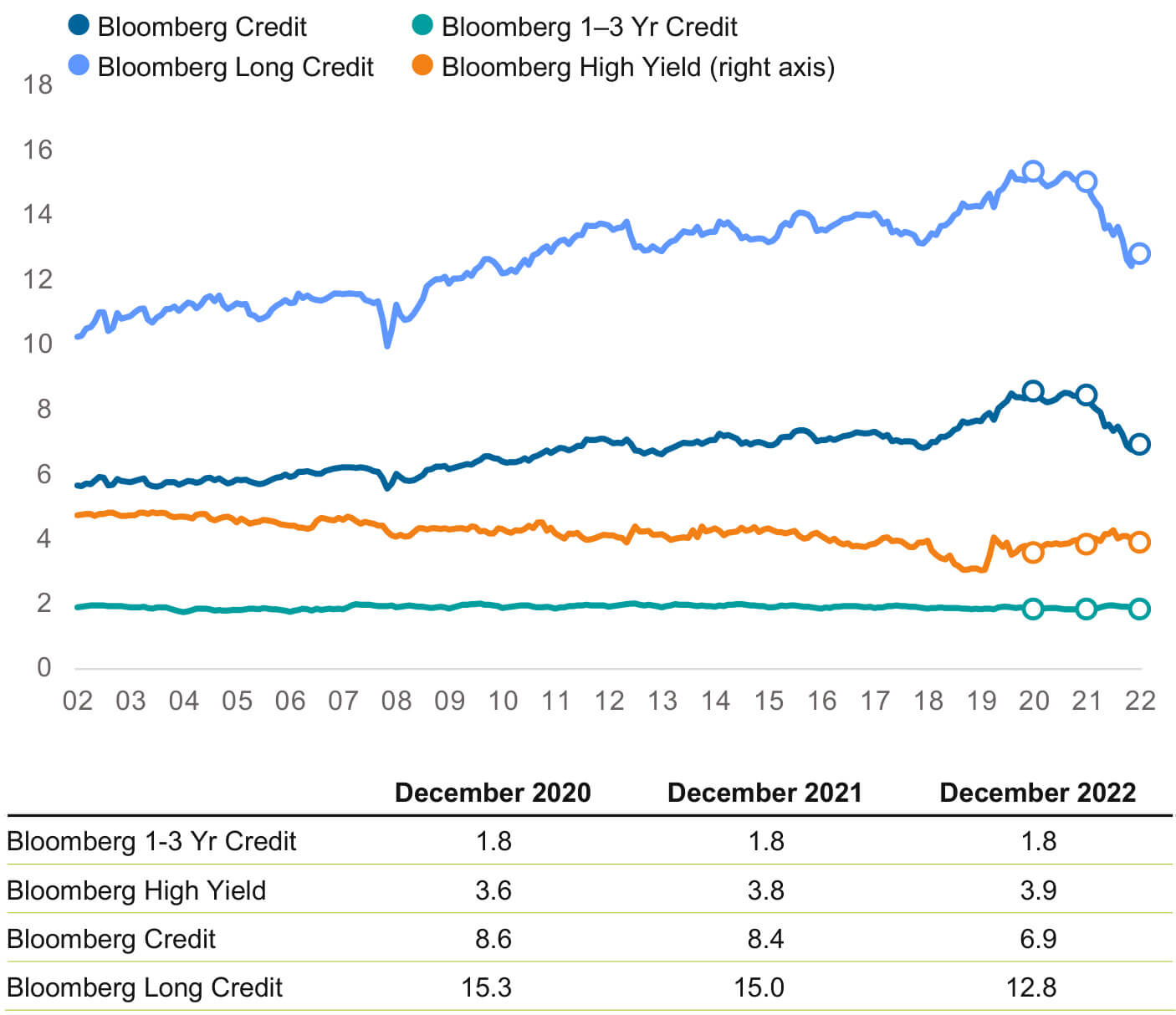

Duration for Intermediate and Longer-Dated Credit Still High but Fell Meaningfully

20 years ending 12/31/22

Duration for credit within the Agg is still high in historical terms but fell significantly in 2022.

- The same is true for long credit.

The yield-to-duration ratio has improved across the maturity spectrum.

Historical Duration

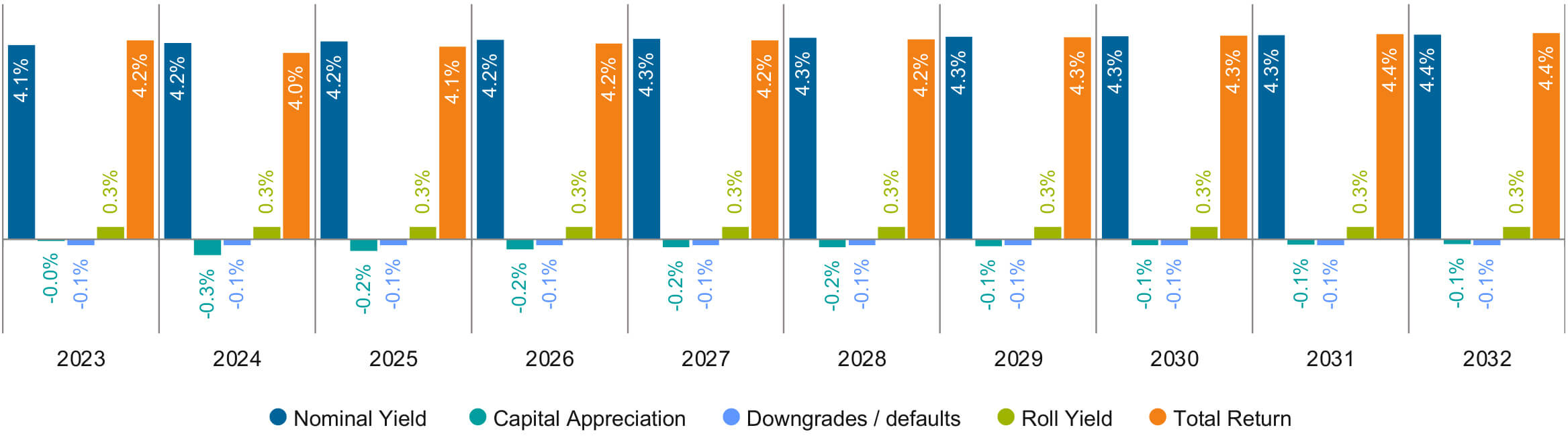

Comparison of Core Fixed Income Return Components

Total Return Attribution: Callan 2023 Projection

Total Return Attribution: Callan 2022 Projection

Equity

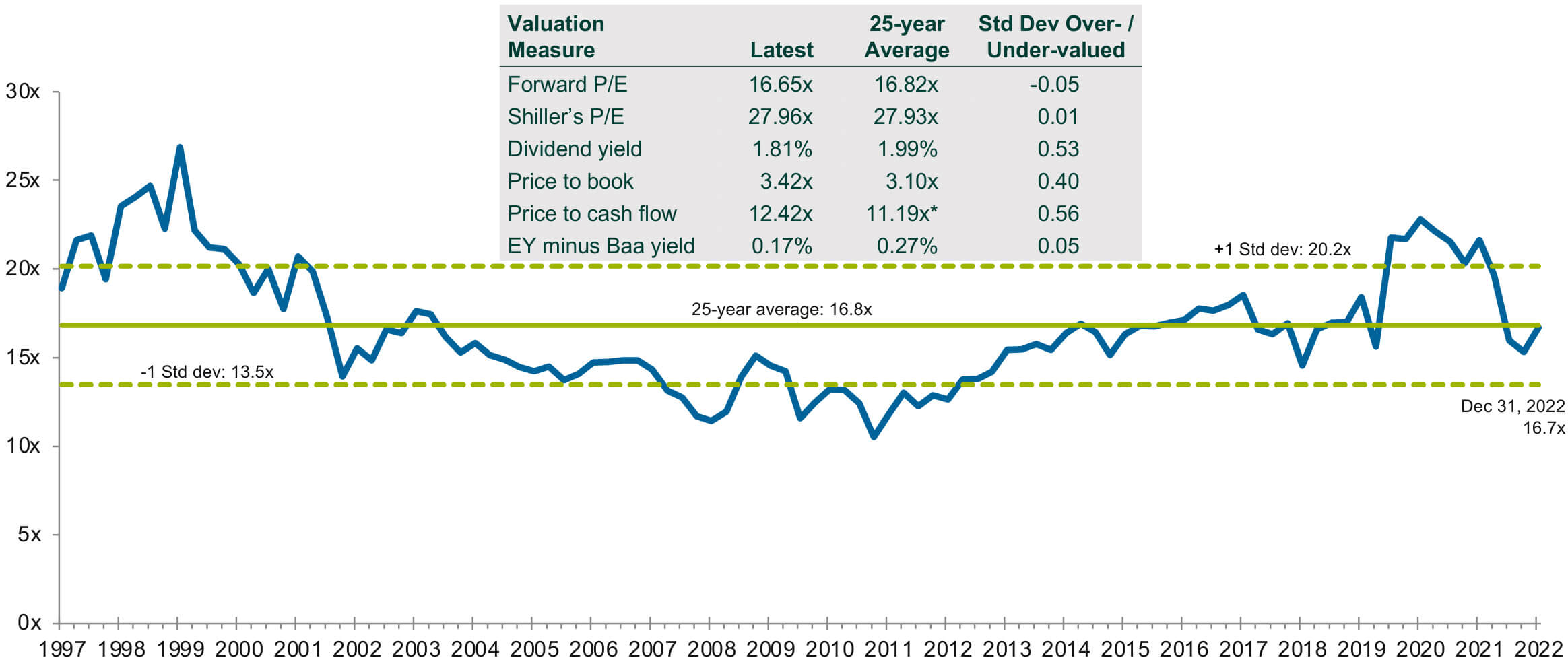

U.S. Equity Market: Key Metrics

S&P 500 valuation measures

S&P 500 Index: Forward P/E Ratio

- All valuation measures are now within +/- one standard deviation of 25-year averages.

- Forward P/E is near the long-term average, but if we enter a recession both prices and earnings are likely to decline.

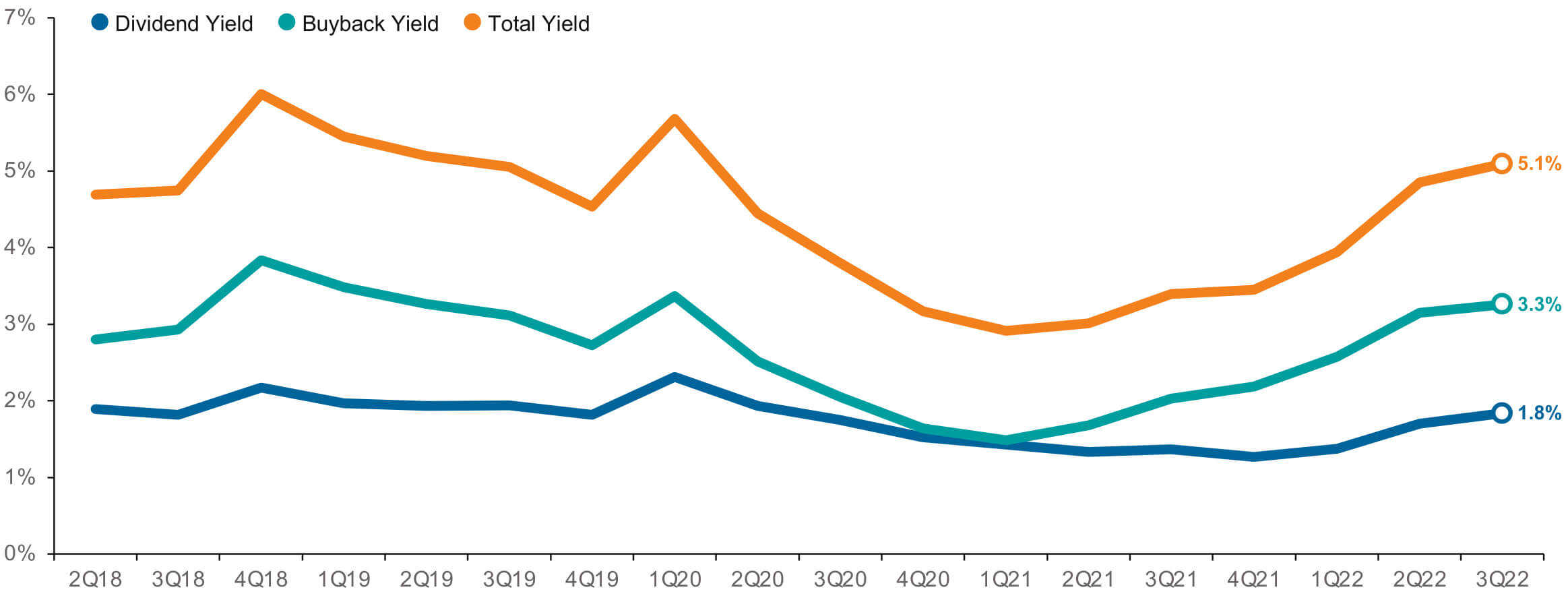

U.S. Equity Market: Return of Cash

S&P 500 yield broken down

Return of cash has risen in dollar terms and yields were further buoyed by declining share prices.

Equity Forecasts

Building blocks

U.S. Equity Assumptions

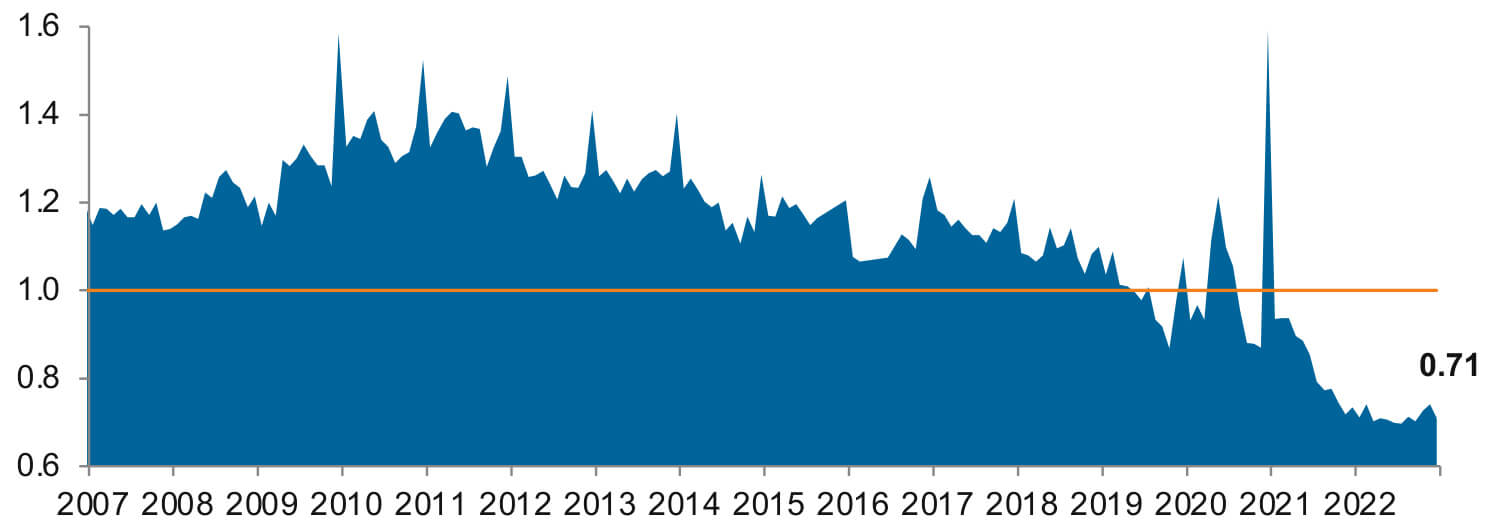

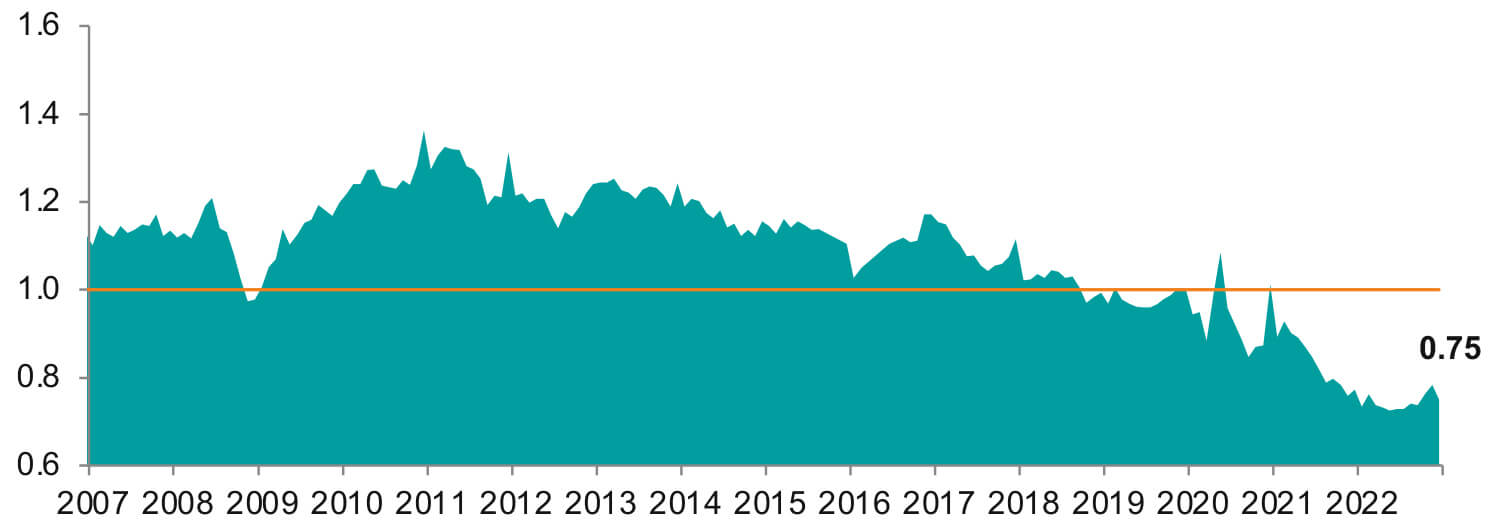

Mid and small cap relative valuations

- Large capitalization stocks still have relatively high valuations.

- Historically, smaller cap stocks have had higher valuations than large caps.

- Investors buying future rather than historical earnings

- The small cap S&P 600 P/E is only 71% of the S&P 500 P/E.

- The mid cap S&P 400 P/E is only 75% of the S&P 500 P/E.

- Lower valuations improve the potential for higher returns relative to large cap going forward.

S&P 600/S&P 500 Relative Forward P/E Ratios

S&P 400/S&P 500 Relative Forward P/E Ratios

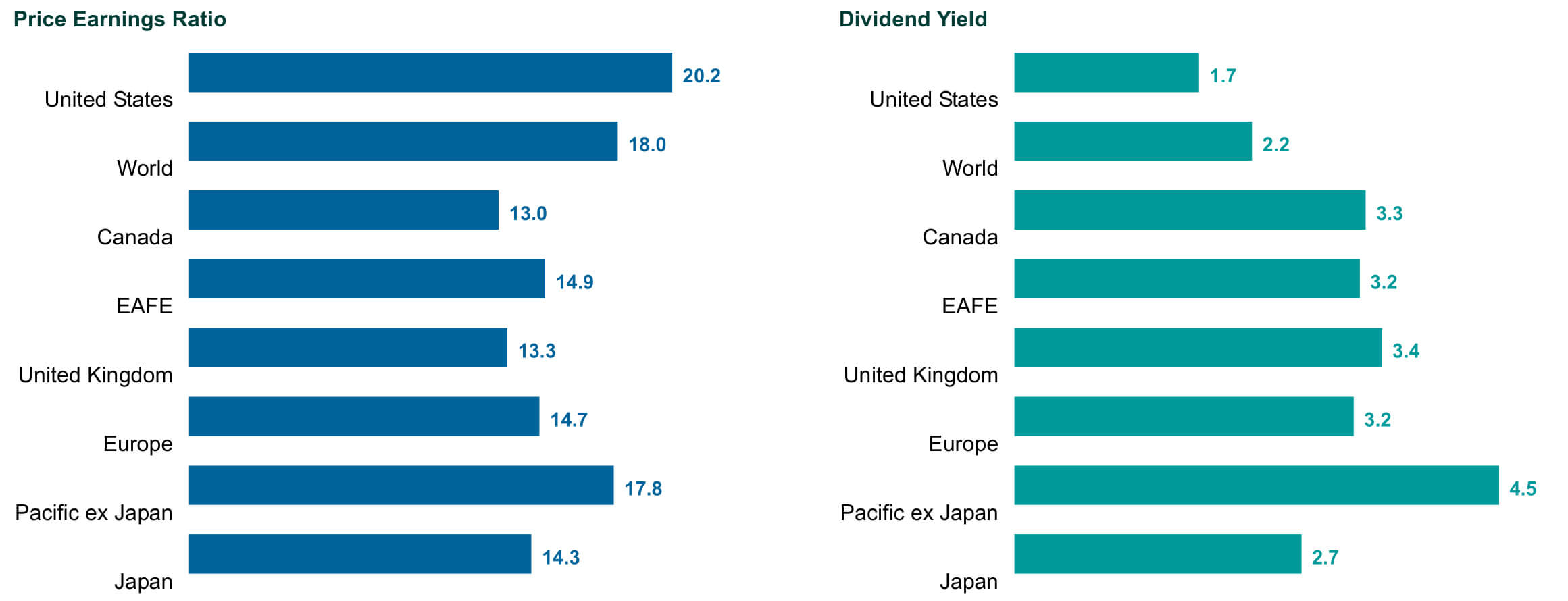

Global ex-U.S. Equity Assumptions

Developed market valuations and dividend yield

Valuations have come down over the past year across each of these developed market indices.

- U.S. continues to have the highest valuations.

Dividend yields have risen since last year for all indices shown except the U.K.

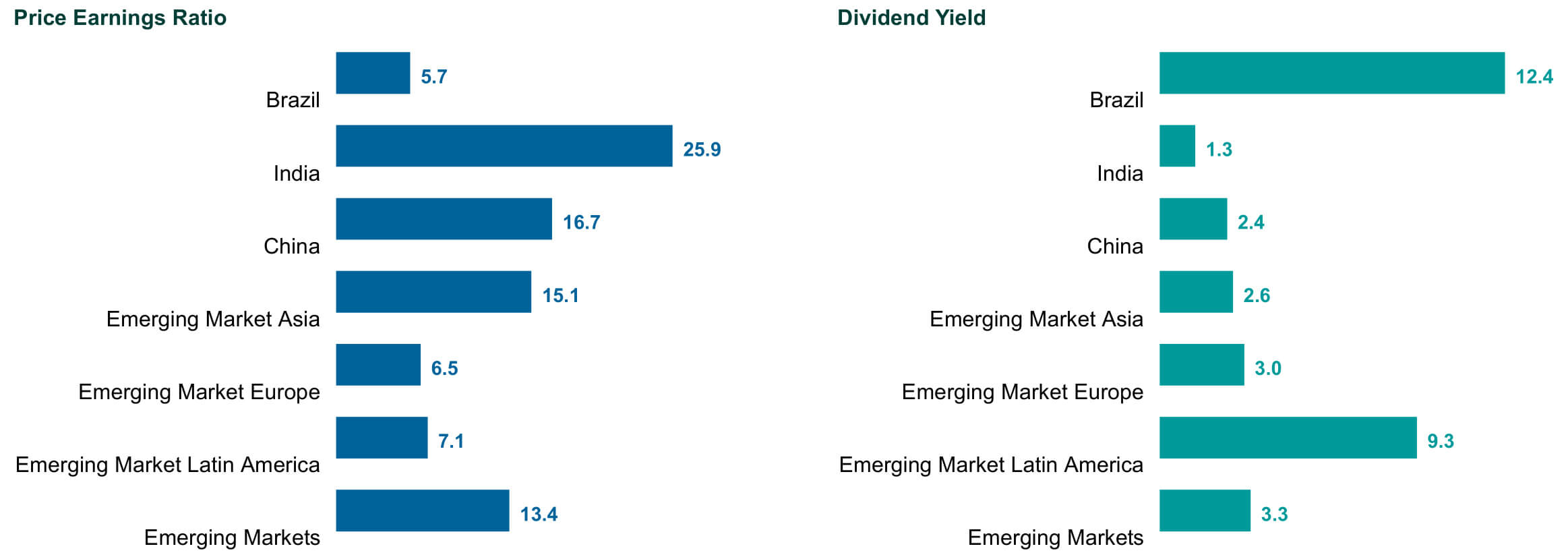

Global ex-U.S. Equity Assumptions

Emerging market valuations and dividend yield

Emerging market valuations have also come down over the last year, but moderately compared to developed market valuations.

- Asia has the highest regional valuations, Emerging Europe the lowest.

Dividend yields have risen meaningfully across emerging market indices.

Significant dilution is realized as growing companies issue more shares.

Equity Forecasts

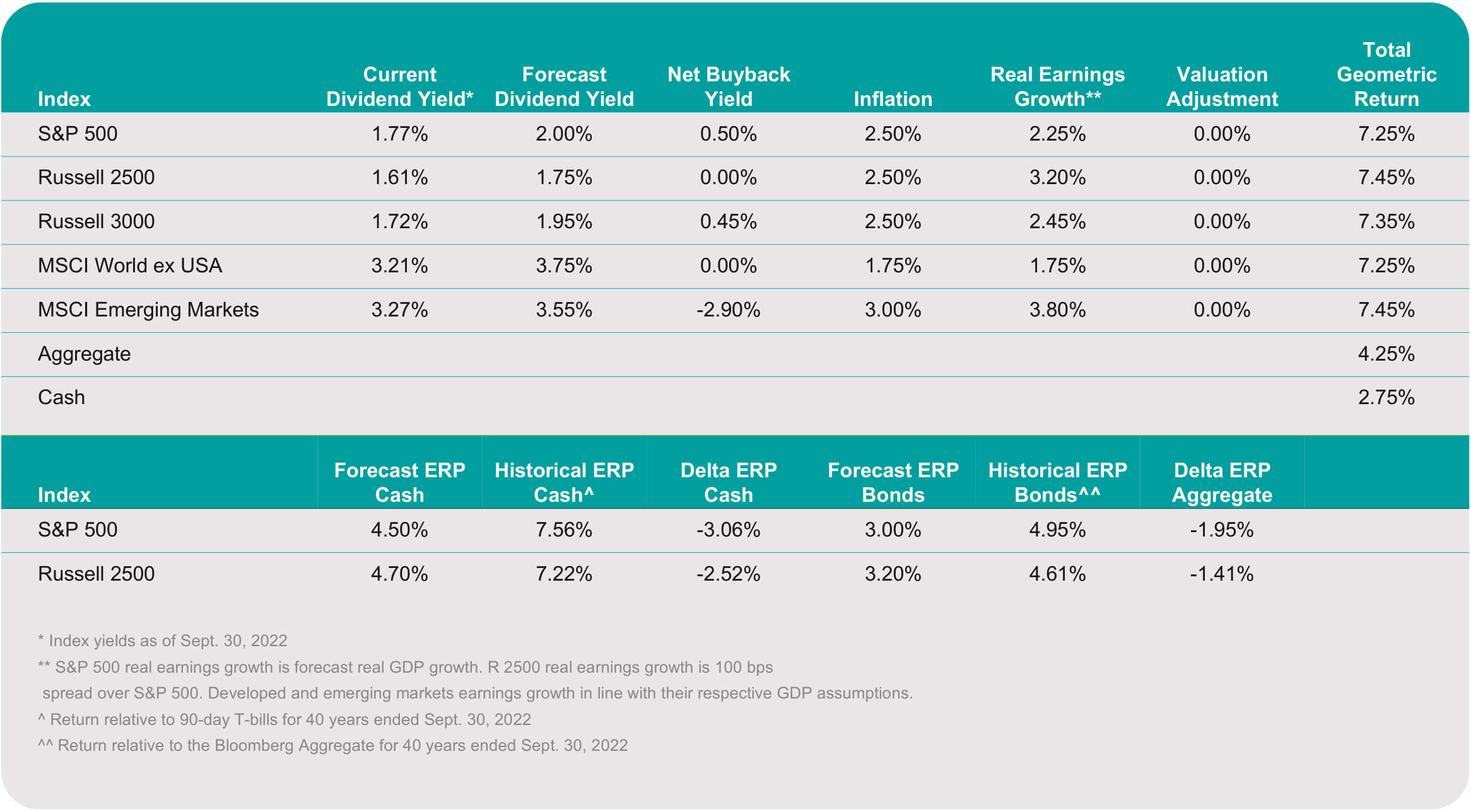

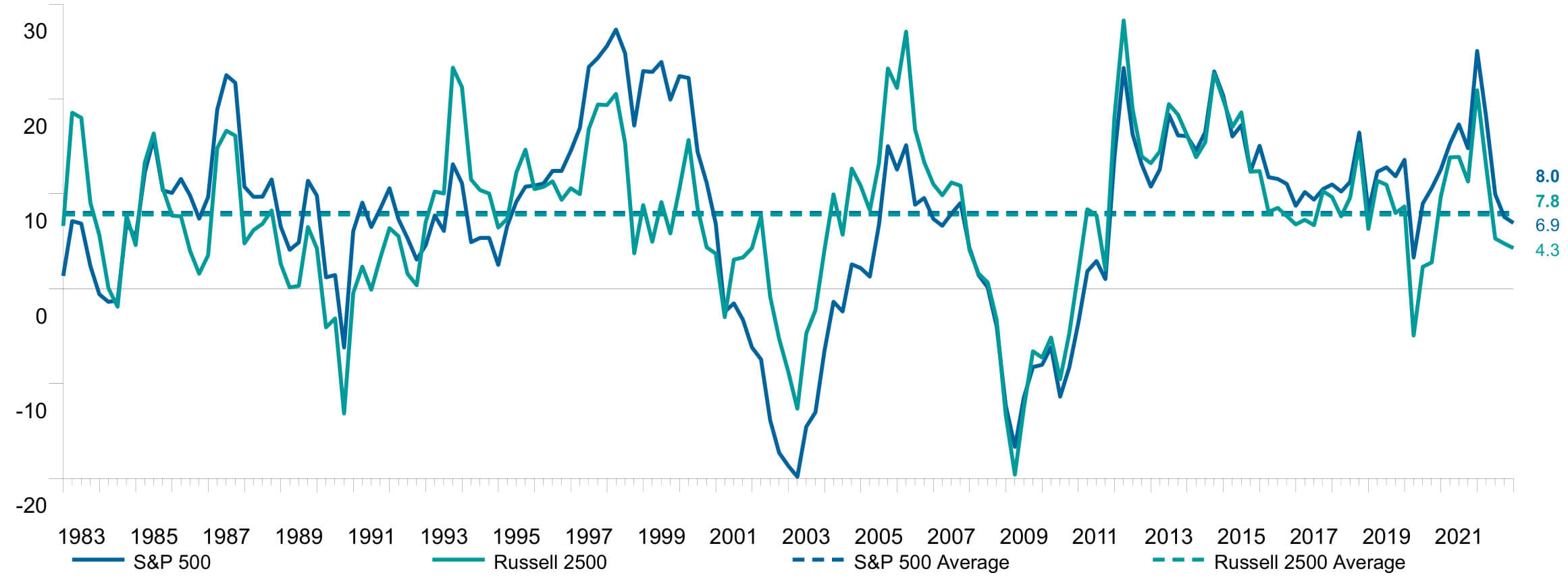

Risk premia over cash

Rolling 3-Year Excess Return Relative to 90-DayT-Bill for 40 Years Ended 12/31/22

Building block approach gives results consistent with an equity risk premium approach.

Alternatives: Focus on Real Estate and Private Credit

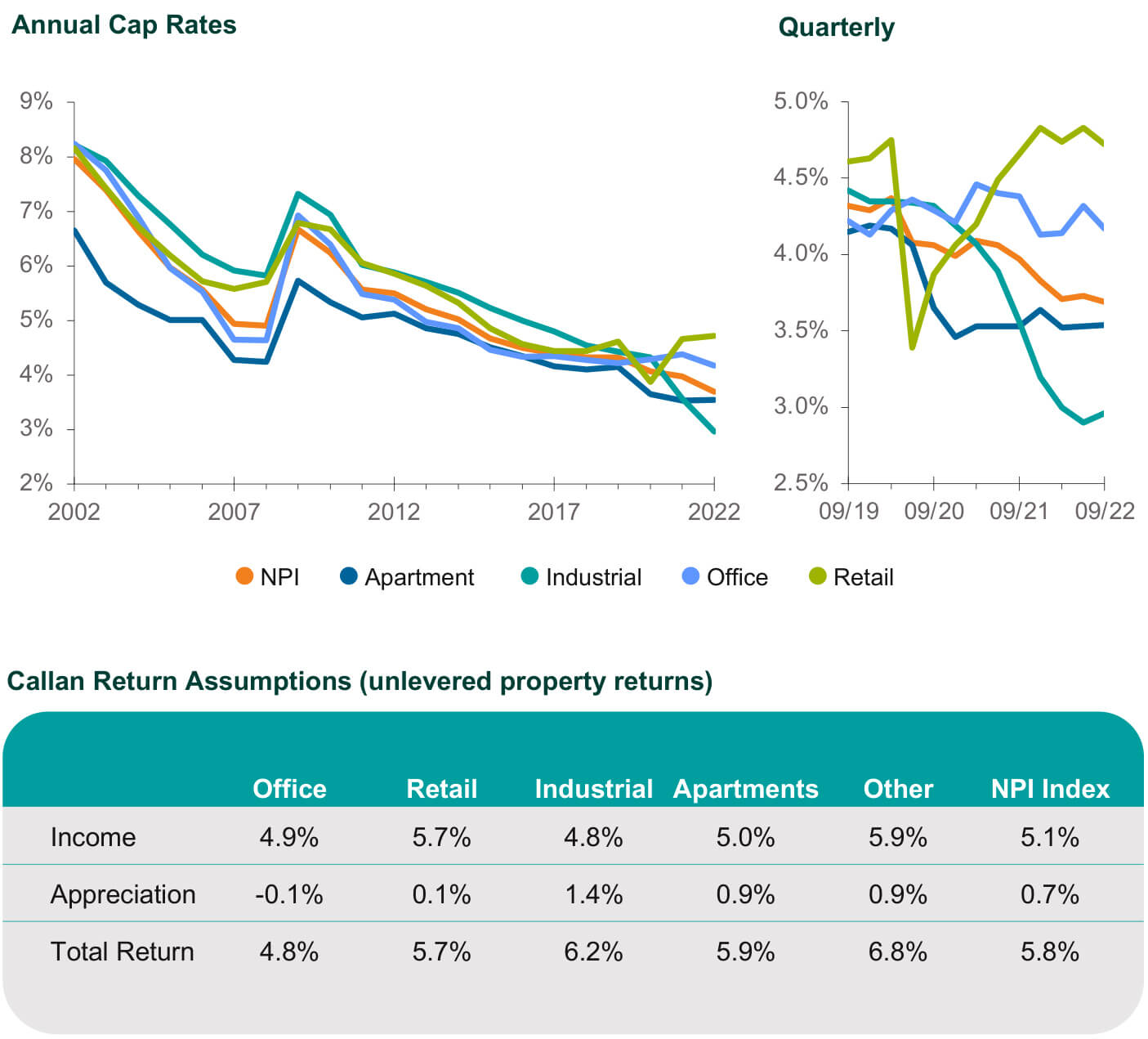

Core Real Estate

- 5.75% core real estate compound return (net of fees)

- Return calculations assume 4.7% cost of leverage and 0.4x debt-to-equity (30% loan-to-value)

Income Return 5.1%

(unlevered property)

Appreciation 0.7%

(unlevered property)

Total Return 5.8%

(before leverage)

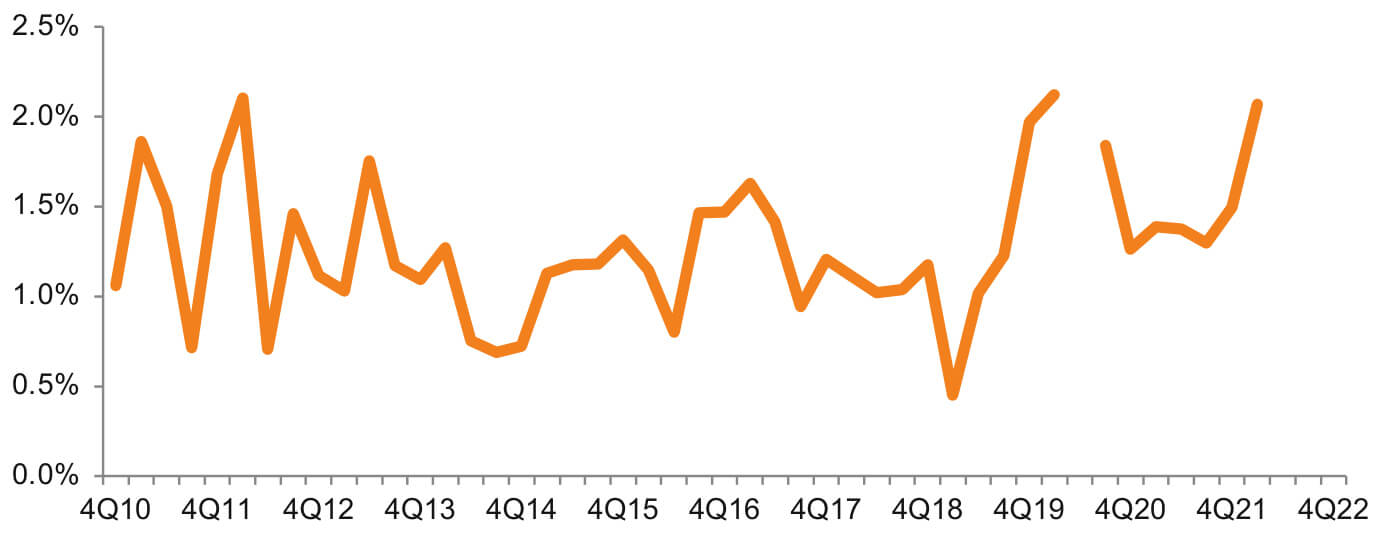

Private Credit

- Return calculations assume 5.25% cost of leverage and 1% unlevered loss ratio

- Corresponds to 7% compound return

| Unlevered Yield | 9.25% |

| Leverage | 0.85x |

| Levered Yield | 12.65% |

| Mgmt Fee and OpEx | 1.7% |

| Incentive Rate | 15% |

| Hurdle | 4% |

| Incentive Fee | 1% |

| Total Fees and Exp. | 2.7% |

| Loss Ratio | 1.85% |

| Net Arithmetic | 8% |

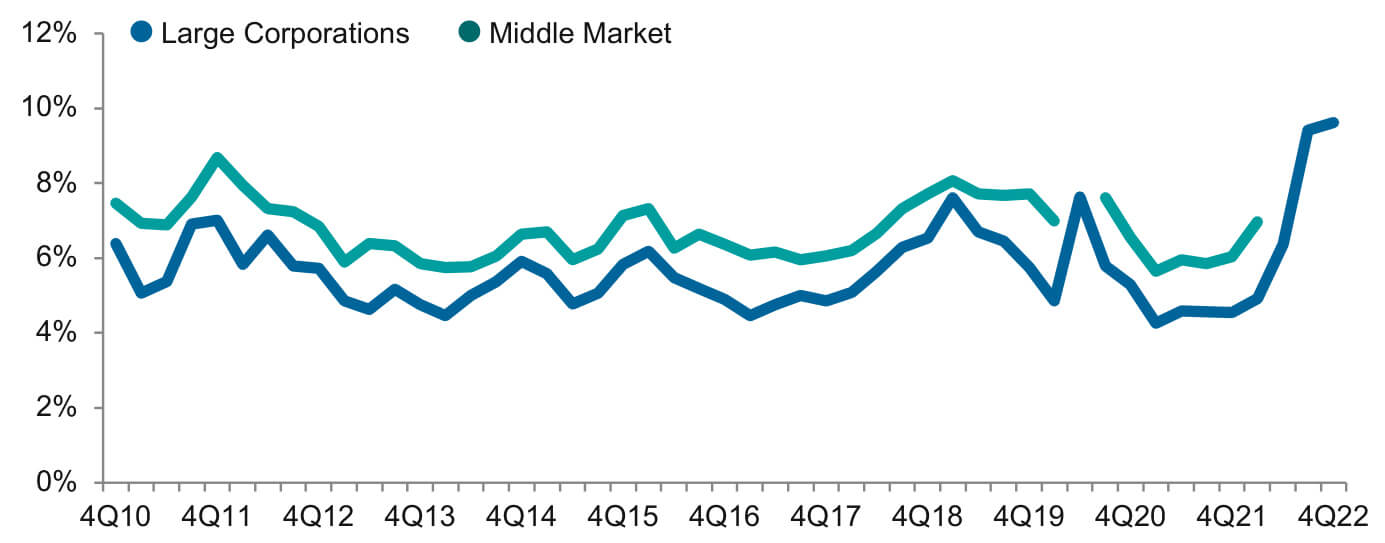

Loan Yields

Middle Market Premium

Detailed 2023 Expectations and Resulting Portfolio Returns and Risks

2023 vs. 2022 Risk and Returns Assumptions

Summary of Callan’s Long-Term Capital Markets Assumptions (2023–2032)

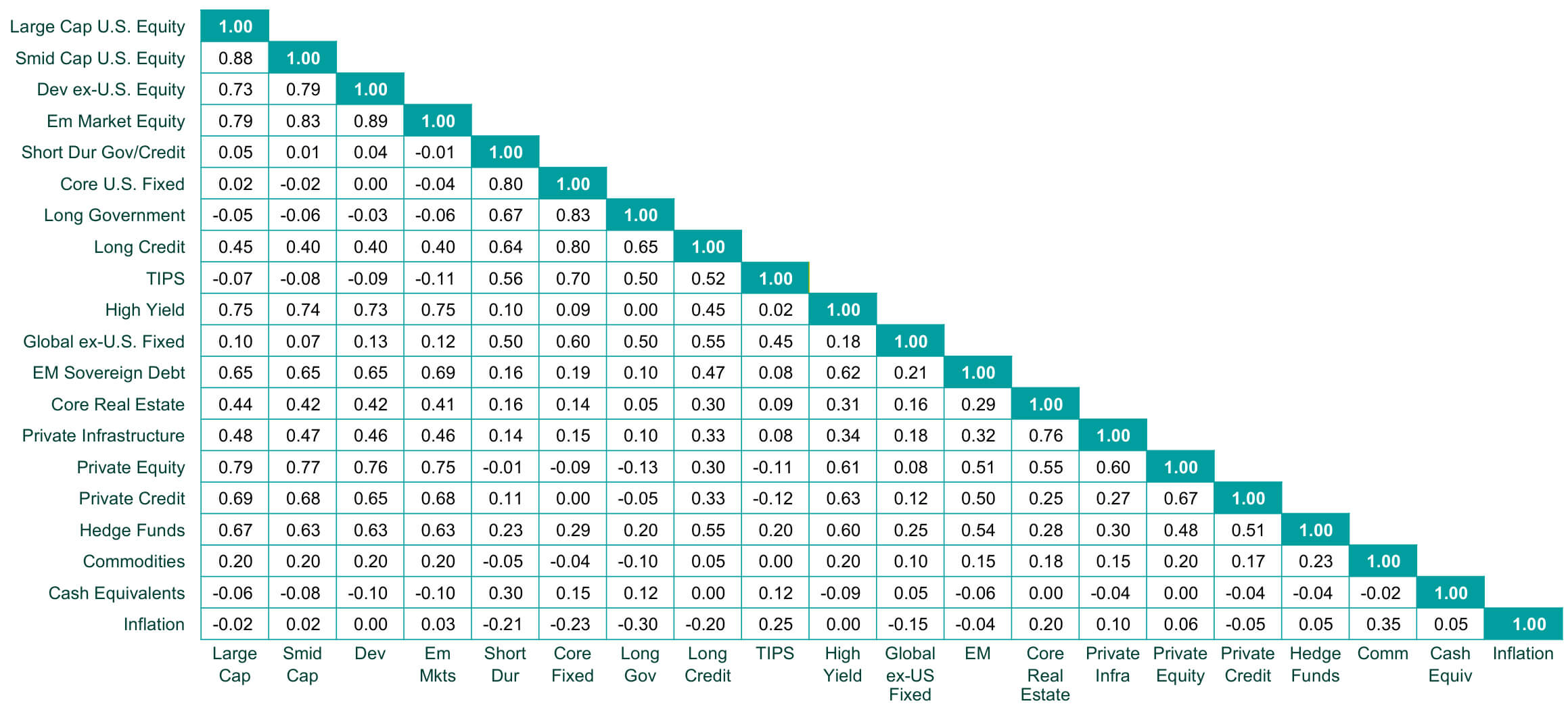

2023–2032 Callan Capital Markets Assumptions Correlations

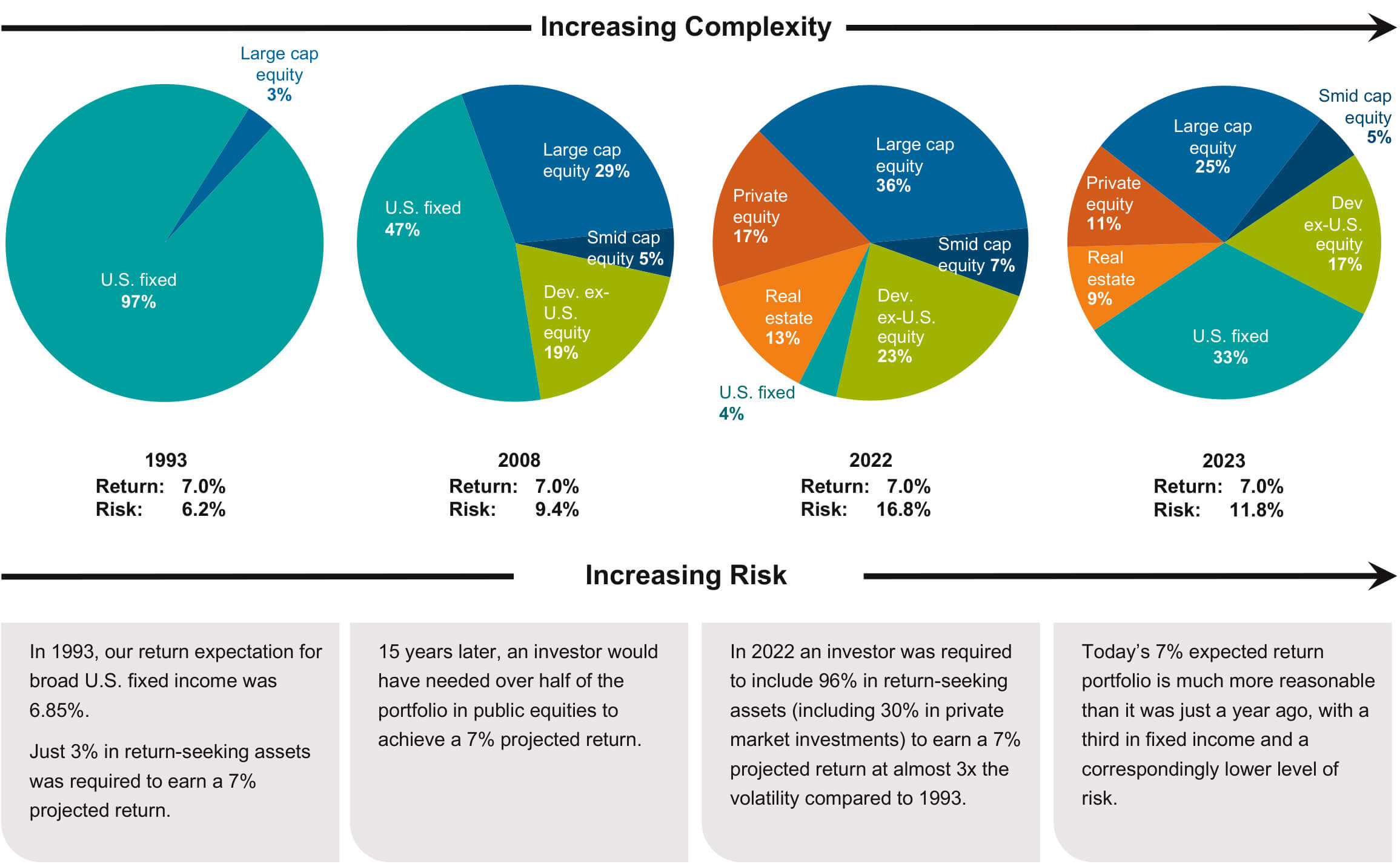

7% Expected Returns Over Past 30 Years

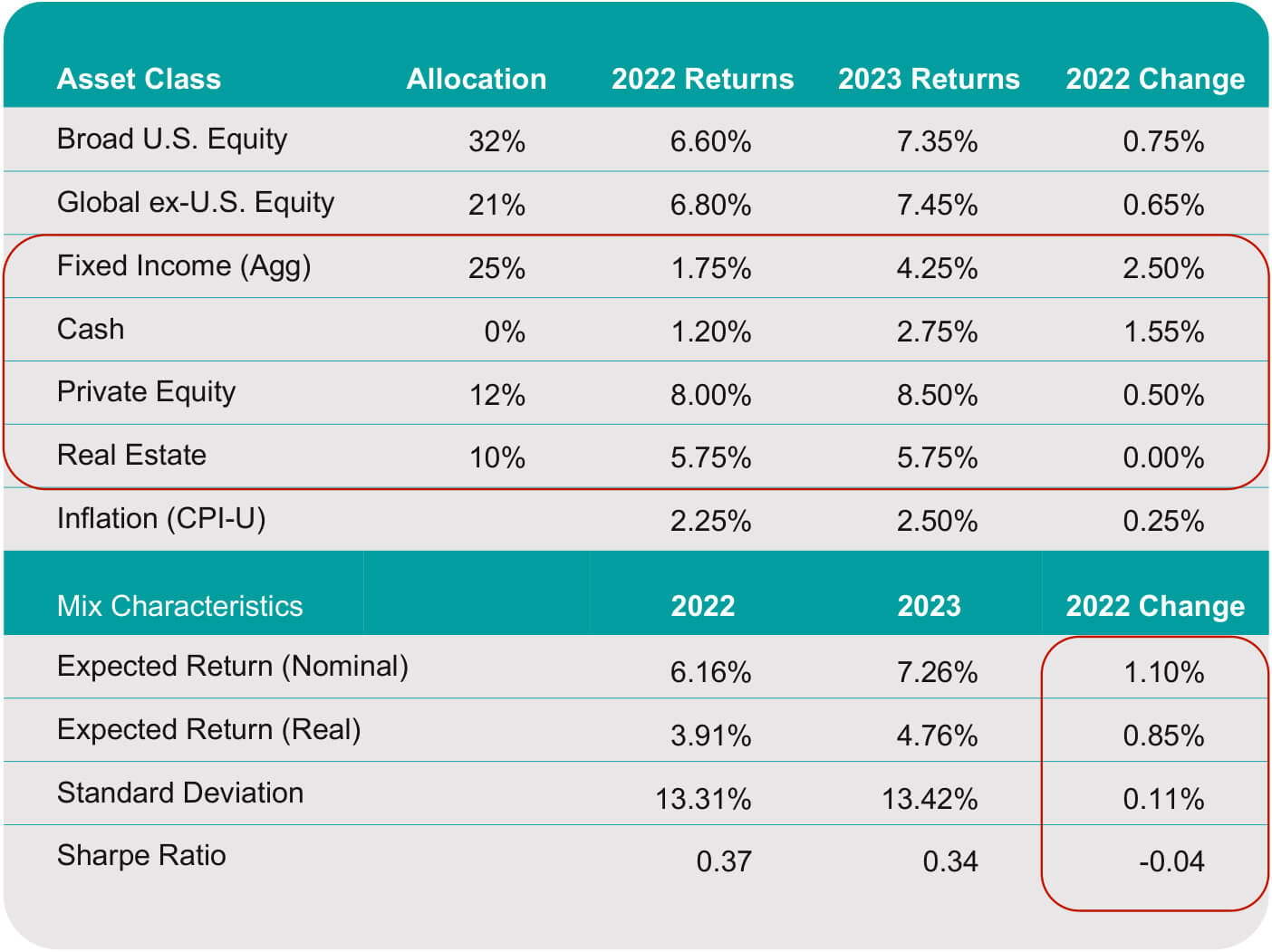

2023 vs. 2022

Typical public DB

Higher risk and return improves nominal return by ~110 bps and increases risk by ~10 bps.

Real portfolio returns are higher in 2023.

Disclaimers

Information contained on this page may include confidential, trade secret and/or proprietary information of Callan and the client. It is incumbent upon the user to maintain such information in strict confidence. Neither this page nor any specific information contained herein is to be used other than by the intended recipient for its intended purpose.

The content of this page is particular to the client and should not be relied upon by any other individual or entity. There can be no assurance that the performance of any account or investment will be comparable to the performance information presented on this page.

Certain information herein has been compiled by Callan from a variety of sources believed to be reliable but for which Callan has not necessarily verified for accuracy or completeness. Information contained herein may not be current. Callan has no obligation to bring current the information contained herein.

This content of this page may consist of statements of opinion, which are made as of the date they are expressed and are not statements of fact. The opinions expressed herein may change based upon changes in economic, market, financial and political conditions and other factors. Callan has no obligation to bring current the opinions expressed herein.

The statements made herein may include forward-looking statement regarding future results. The forward-looking statements herein: (i) are best estimations consistent with the information available as of the date hereof and (ii) involve known and unknown risks and uncertainties. Actual results may vary, perhaps materially, from the future results projected on this page. Undue reliance should not be placed on forward-looking statements.

Callan disclaims any responsibility for reviewing the risks of individual securities or the compliance/non-compliance of individual security holdings with a client’s investment policy guidelines.

This page should not be construed as legal or tax advice on any matter. You should consult with legal and tax advisers before applying any of this information to your particular situation.

Reference to, or inclusion on this page of, any product, service or entity should not necessarily be construed as recommendation, approval, or endorsement or such product, service or entity by Callan.

This page is provided in connection with Callan’s consulting services and should not be viewed as an advertisement of Callan, or of the strategies or products discussed or referenced herein.

The issues considered and risks highlighted herein are not comprehensive and other risks may exist that the user of this page may deem material regarding the enclosed information.

Any decision you make on the basis of this page is sole responsibility of the client, as the intended recipient, and it is incumbent upon you to make an independent determination of the suitability and consequences of such a decision.

Callan undertakes no obligation to update the information contained herein except as specifically requested by the client.

Past performance is no guarantee of future results.